Conversational banking – How KB is shaping the future of banking

How did a seemingly small idea – replacing SMS with IP messaging in a banking app for a developing country – lead to the fundamental transformation of digital banking built on chat as a platform?

This is the arc of Kookmin Bank’s (KB) digital banking transformation. It led to in-app chat becoming the center of KB’s platform strategy for shaping online and mobile banking into an interactive and conversational user experience.

KB Financial Group – Pioneering mobile banking

KB Financial Group is the largest financial institution in Korea with total assets exceeding $434 billion. Currently, their portfolio has been diversified into 20 financial subsidiaries including KB Bank, KB Card, KB Asset Management under the umbrella of KB Financial Group

Since 2016, KB has pioneered its mobile banking platform with emerging technologies (e.g., blockchain, AI, chat interface, and more) and rapidly replaced its legacy systems with the Liiv brand. These interet specific banking brands, like Liiv and Liiv Mate, launched in Korea early in 2017. KB released its global banking expansion into Cambodia, where it applied messaging experiences, first, to replace the costly SMS and, second, to drive the digital transformation of its banking.

The opportunity: Meet millennials online, while increasing profit and shifting operational excellence to mobile

For a long time, banking services centered around offline interactions – local banking branches, phone calls or telephony, and time consuming consultations on complex financial products. Now, it faces the hurdle of serving millennials, the dominant and emerging digital customers.

Conventional banking is now pushing hard to complete its digital transformation because it is suffering in two major ways: (1) from the poor implementation of its online and mobile transition and (2) from the deteriorating profitability and operational excellency of its offline branches.

KB’s Global Banking: Geographical expansion and chat as the backbone of its communication infrastructure

‘KB Global Digital Bank’ is a diverse mobile banking service designed to make digital banking accessible to everyone. KB built it on a rechargeable wallet system and the integration of chat and messaging. It offers money wiring, overseas money transfer, and peer-to-peer (P2P) payments.

KB Financial Group was targeting overseas markets. Knowing that security and financial regulations can vary widely from country to country, KB sought partnerships with fintech companies that directly addressed these problems to avoid any friction when entering a foreign market. Language barriers and cultural differences also provide serious challenges to overseas expansion. Face-to-face interactions, like in consumer banking, can exacerbate these cultural and linguistic differences even further. KB’s solution used mobile banking with messaging as an integrated communication channel to address both cultural and linguistic barriers. The result was KB Global Digital Bank.

The Korean market has an extremely high penetration of mobile messengers and Kakao especially. It accounts for 94 percent of the mobile population in the country. In May 2017, Kakao tried to enter online online banking, potentially posing a threat to KB’s market with a highly popular technology. To respond to Kakao’s forays into mobile banking, KB responded by integrating messaging technology into its business in Cambodia, where the region has similar mobile use behavior.

Cost, too, played a part in choosing messaging technology for the Cambodian market. In Cambodia, KB initially thought to send SMS to its customers for all messages, including information about transactions. However, they soon discovered that the cost was far more expensive than IP messaging for both consumers and KB. Given the characteristics of Cambodia’s mobile population and the cost-efficiency of IP, instant messaging became a clear potential keystone for KB’s communication strategy and they began reviewing SendBird as a result.

Communicate seamlessly with buyers.

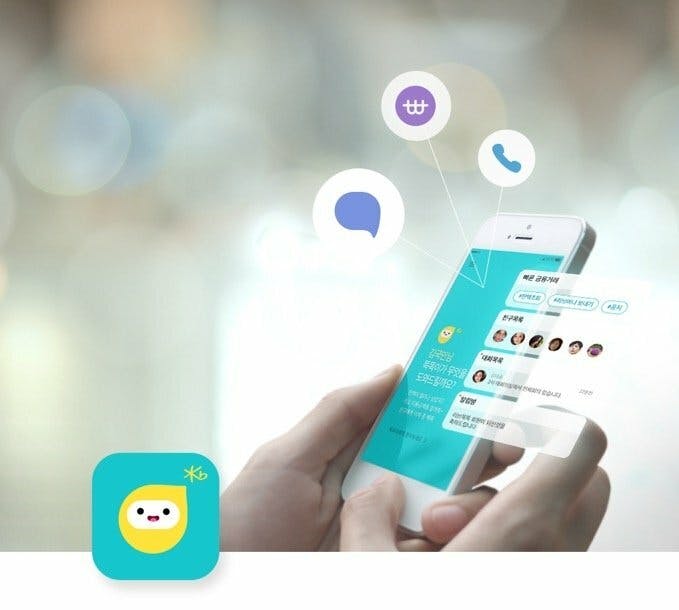

Liiv Talk Talk – Conversational Banking becomes the platform for consumer finance

After selecting messaging as its platform, conversational banking became interactive banking. “The key differentiator of Liiv Talk Talk is how we designed the Talk Talk agent to be the gateway for the conversational experience as both a chat customer support agent and a concierge system,” says Hyungju Park, the general manager of the Smart Strategy Department of KB, “A customer, less familiar with an online, non-face-to-face service, can intuit the key goals of the service and explore its features more naturally by engaging the Talk Talk agent.”

For further conversational banking automation, check out our AI concierges.

Conventional online and mobile banking services, on the other hand, experienced drawbacks when customers needed to explore the services activated by a complex UI, menu, and set of products instead of simply asking a teller or an adviser. KB, therefore, elevated the messenger to the center of its application so that it could implement a conversational, seamless user experience similar to that of the conventional bank teller at an offline bank branch.

KB Liiv Talk Talk also enabled a chatbot with machine learning for its concierge agent, Talk Talk, to personalize the user’s experience and give them immediate responses to their inquiries – more quickly than other mobile banking services. It also offered a commenting system and streamlined popular services by using command line functions for transferring money, looking up accounts or pension funds, and managing credit card accounts by simply using buttons like #, @, ₩.

Another common scenario that KB addressed with messaging was services for multiple simultaneous customers seeking, for example, joint mortgages for joint tenancy. In KB’s Liiv Talk Talk, you simply invite your friend or partner to a chat room where you both consult with a KB Agent. The chat room itself asks you and your partner for consent on a specific mortgage and then proceeds for approval. This is one of the most unique values of conversational banking – enabling a transaction across multiple participants at once, whereas typical online banking only offers 1:1 transactions.

KB also integrates its marketing messages and system notifications into a single chat channel. Previously, all KB’s messaging channels were highly fragmented and relied heavily on SMS. It was difficult to track interactions from medium to medium and didn’t lead to user retention (because users had to leave the app). Nor did it engage millennials, who often decline to respond to SMS or voice calls. For KB messaging killed two birds with one stone. KB Bank wagers that instant messaging will give them a richer connection to the SMS- and Voice-averse millennials while successfully integrating all their messages into a single channel.

The end goal is to transform Liiv Talk Talk into a consumer banking platform while integrating every banking and financial service as an API so customers can use the service as the central hub for their every financial need. To realize this prospect, KB is investing in this strategy and applying conversational services to its credit card subsidiary, KB Card. It offers a conversational membership platform, KB Liiv Mate, to manage the mileage and loyalty programs and subscriptions into a single channel.

Technical challenges banks may face and how KB is solving them

Like in many countries, the banking industry in Korea is highly regulated and other banks might perceive obstacles to moving their system and data to the cloud. To address this serious concern and many others, KB not only needed to build a server architecture to comply with regulations, but they also needed to be agile enough to proactively address potential concerns. This latter point, KB wagered, could be a great way to differentiate itself from other more conservative banks.

Hybrid cloud infrastructure

The backend system of Liiv Talk Talk is integrated between AWS's cloud infrastructure and KB’s on-premise servers. So, inside the hybrid cloud structure, the messenger runs on top of the AWS Cloud while it calls all the bank’s user data, including financial information, from KB’s local servers.

This division between the cloud and local servers helps facilitate both security and performance. In-app messaging and web-based services have different architectures. It’s relatively easier to estimate the user behavior and traffic of web services compared to a messaging service. Anticipating data-heavy and yet common messaging behaviors, like uploading pictures or videos, can make predicting traffic or data use even more challenging. Consequently, KB calls user data from its local banking server so neither service interferes with the other.

Investing in NLP for a seamless chatbot integration

Investing in Natural Language Processing (NLP) technology could be another challenge and is the core of KB’s chatbot implementation. To make this conversational banking service seamless for the user, it’s integral to upgrade one’s associated NLP technology. KB addresses this technical challenge by narrowing the focus of its NLP training. Rather than training its bot on all user conversations, KB focuses its NLP on data specific to the user requests from its affiliated financial services. It expects to accelerate this initiative and launch publicly in early 2019.

Organizational challenges – Becoming Agile

To address the need for cutting-edge technology and the requisite speed to implement it, KB adopted a new organizational experiment called, Agile Squad. It is responsible for developing Liiv Talk Talk and KB’s upcoming banking services. Agile Squad is a group of 5-6 young, talented people. It is designed to deliver projects spinning off of the conventional banking organization and to encourage and enable faster decision-making with respect to the evolution of IT/Mobile banking.

Thanks to Agile Squad, KB was able to complete its application development for Liiv Talk Talk in three months and able to provide a feature update as frequently as every month. Although it’s typically rare to have such a team in a conventionally conservative industry like banking, the IT industry sees great success with similarly organized teams.

Identifying and investing in the right technology

KB also established its corporate venture arm, KB Innovation Hub, as a startup accelerator and opened the KB Fintech Hub Center to identify and adopt best-in-class technology partners, like SendBird. So far, KB Innovation Hub has partnered with 36 startups and provides extensive support, such as co-working spaces, co-business case development, investment, and opportunities for carrying out the front line of R&D throughout its organization.

Conversational banking is the dominant trend of major banks worldwide, and many experiments have been conducted to implement messaging services and AI-powered chatbots as an integral part of banking’s future.

Conclusion: In-app messaging must replace Messengers

The key is to ask how you can connect and interact with digital customers using your existing service and not hope or expect that consumers will one day flock to your existing solution and user experience. Many banking solutions use third-party messengers like Facebook Messenger, hoping to optimize the experimental cost of conversational banking. But with this minimal investment, they’re experiencing poor results and a similar user experience. Facebook has shown time and again that it isn’t a good long-term solution for integrating messaging into your services.

The banking industry must now take ownership of its messaging experience and leverage that data to deliver outstanding user experiences with NLP and live agents alike. Facebook also tried to offer structured messaging as a way to commoditize chatbots and conversational commerce for as many verticals as possible. But the effort failed because every use case and industry requires a customized solution based on its app, services, and brand.

Conversational banking integrated into a bank’s app can offer the right level of customization to optimize your user experience while limiting the investment in building the solution in-house.