Lessons from fintech for legacy financial firms

In recent years, fintech has seen massive growth, with the number of fintech startups having doubled since 2019, according to Statista.

Even non-financial companies are getting into fintech, as seen with Adobe’s recent announcement of its plans to launch a payments service.

Consumers have embraced fintech, it is becoming an essential part of daily life. A 2021 Blumberg Capital survey found that a majority of consumers (66%) believe that fintech solutions are a necessity for personal finance, not just a nice to have.

If the everyday consumer is increasingly aware of the benefits fintech provides, it is necessary for legacy banks to adapt to shifts in the industry.

It’s no longer enough to digitize the financial transaction. Consumers expect the interactions that support those transactions–think financial advice or customer support–to be digital as well.

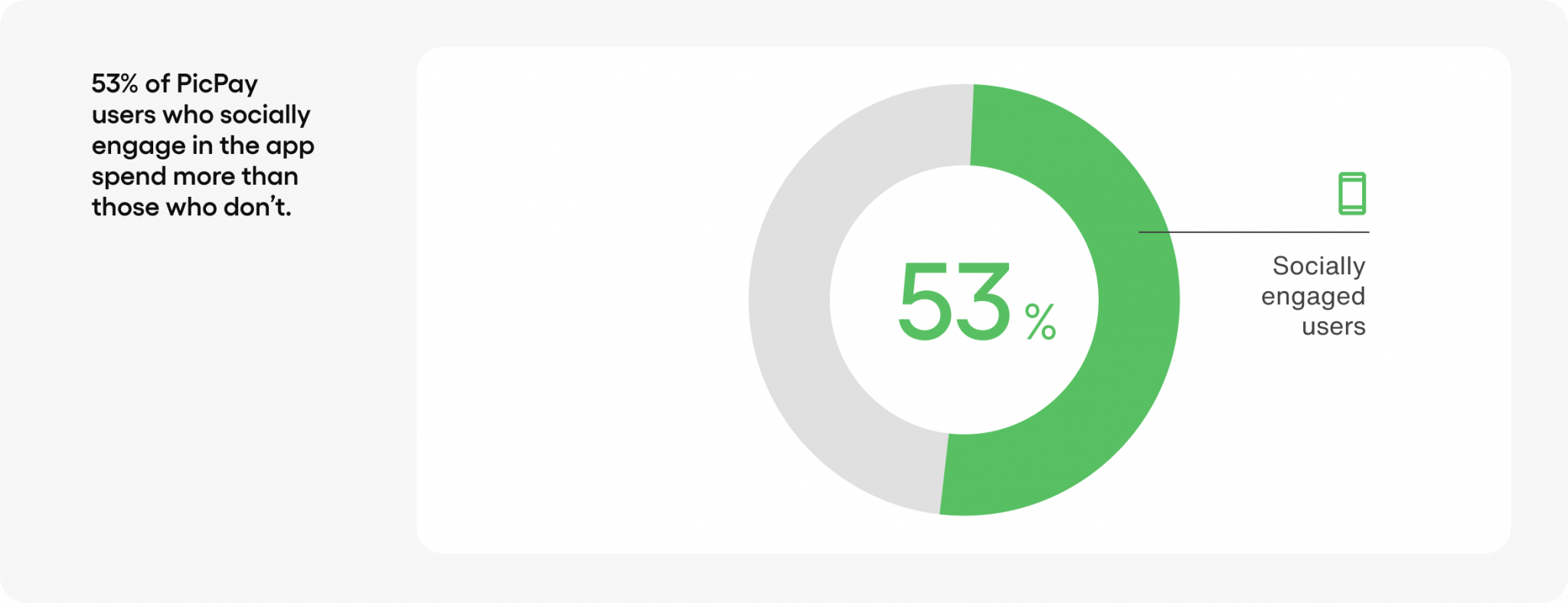

Members of highly engaged communities are inspired and fired up by their interactions with other members, and when they’re fired up about something, they talk about it. Participating in these communities with your financial app makes users feel like they’re part of something bigger.

The rise of fintech

One of the key drivers of fintech’s growth is that consumer expectations are changing, and new financial and technological advancements are emerging to address these evolving needs.

Fintech often targets consumer needs that aren’t being met by existing financial service providers. Many of us have come to prefer the ease, convenience, and security of mobile banking and payment options–which is also why we see shifts from payment hardware to payment software.

New fintech startups are also able to provide services that keep customers socially engaged. Beyond building trust through messaging, many neobanks offer guidance to personal finances and services, digitally.

Legacy infrastructure can make these changes difficult to adopt. However, while it’s true that legacy financial service institutions like banks tend to be less agile than their new competitors, there is much they can do to better meet today’s consumer.

Below, we’ll discuss the factors that drive fintech’s success and how traditional financial companies can respond.

Modern branding and user interface design

Fintechs put a lot of thought into their user interface design to deliver painless and familiar user experiences that make it as easy as possible for customers to use their services. While the services they offer may use the same back-end processes as more established banks, fintech apps tend to be more simple to navigate, and their simple branding and design elements make them visually appealing and inviting to consumers.

Simplified branding and user interface design is what fintech apps are known for, but you can take a chapter from their book with our UI design kit. Create user experiences that enable customers to perform actions as easily (with as few clicks or taps) as possible. Including features like data visualization dashboards can help users to gain insight into their financial situation at a glance, adding value.

Connected customer service

Leading fintech apps are putting their mobile experience at the center of their customer relationships. Instead of having to pick up a phone or submit a claim via email, customers can handle support issues or questions using the app.

This also makes it convenient for companies to reference previous issues quickly.

When consumers research and weigh different financial products and services, they should find easy-to-understand information, visual comparison tools, and have on-demand access to Help resources when they need them. This can take the form of self-service resources like FAQ pages, informative blogs and videos, helpful email communications, community forums, and/or direct access to product experts through tools like in-app chat.

Consumers often have questions related to a purchase from a business. Supporting in-app messaging between the consumer and a business around a payment made with your service engages both sides beyond the transaction.

Communicate seamlessly with buyers.

Financial planning and advice

Many fintechs offer features that add value to their services and help their customers to achieve their goals. This can take the form of features or pricing models tailored to customers’ lifestyle and changing needs, or resources like financial education, communities of like-minded individuals, or personalized tips, services, and product recommendations.

These offerings help customers to hit their financial targets, whether it’s sticking to a budget, saving towards a goal, learning about investing strategies or making an essential purchase more manageable (as is the case with interest-free BNPL services).

As consumers become more financially empowered, in part due to the rise of social finance, they’re less likely to rely on financial advisers and more likely to seek financial products and services they can use independently. When questions do arise, they’ll expect to find self-service tools, on-demand assistance, and communities where they can learn from successful users.

Transparency and trust

One of the key ways fintechs attract and retain users is through transparency and clear communication. Clarity builds trust, particularly among younger consumers for whom understanding terms and conditions is increasingly important, and who are easily put off by opaque policies and vague pricing information.

A transaction is the simple part. Customers want more than that: to engage with you, express their opinions, and share their experiences. According to research from Capgemini, feelings of trust, familiarity, belonging, and security have the strongest correlation with loyalty.

Trust is a big one. In order to power secure in app chat, Sendbird relies on identity-based security where customers and merchants create a secure and authenticated profile in your app. Identity adds a layer of security in that users can block other users and confirm a person’s identity through both the chat and financial institution. This will build trust for peer-to-peer (P2P) and consumer-to-business (C2B) payments.

More agile tech stacks

While many established financial services providers are still struggling to implement digital transformation initiatives to bring their operations into the 21st century, fintechs are basically synonymous with digital banking. Fintechs are increasingly offering innovative features like AI-powered transaction categorization, automated investing, personalized financial tips, and social features like activity feeds and in-app messaging capabilities.

A big part of the reason fintechs are able to roll out new value-adding features with ease is their use of application programming interfaces (APIs), which allow them to plug ready-made features into their existing architecture. Companies are choosing to buy, then build, an approach that enables them to select best-in-breed features instead of using valuable developer resources building from scratch..

How legacy financial firms can survive the fintech boom

Every company requires a digital strategy to remain competitive. Remaining stuck within legacy systems can lead to higher operational risks and poor customer experience. Ramping up in-app solutions and payment methods digital services and updated payment methods is the key to standing out in this competitive landscape.

If your customer has gone digital, you must as well. Providing customers with a digital banking and service option isn’t a nice-to-have anymore, its a necessity. Legacy banks should invest in single-source-of-truth knowledge bases and customer service training; easy-to-understand self-service resources and chatbots; support automation tools that escalate queries to human support agents; well-equipped social media teams; and features like messaging that facilitate human in-app support; and better customer support experiences through always-on support conversations.

In-app messaging between users provides the ability to have conversation and context around a payment with a peer or group of peers. Connecting your users to each other at scale makes them feel a part of something larger. If you provide your customers with access to a community they relate to and resources that make their lives easier, they’re more likely to be loyal.