Welcome to the age of personalized banking

39% of consumers say that they are more likely to use banking services from a fintech company thanks to COVID-19, according to financial data platform MX.

Fintechs, neobanks, and cloud banks are soaring in popularity because they provide a personalized, omnichannel experience. To compete, traditional banks need to adopt the ubiquitous access of fintechs and rethink their digital strategy.

Most banks in North America have already made the switch to digital, but that’s not enough. With the entry of fintech comes an increased demand for hyper-personalization—the need to tailor your banking experience to specific customer segments and individual customer needs.

Conspicuous consumption and the role of big data

There was a time when talking about your personal finance was considered taboo. But today, with the amount of data that’s freely available on the internet, that’s changed completely.

Conspicuous consumption—buying something to display one’s wealth and elevate one’s financial status—has become more commonplace than ever before. It has given rise to this new age of purpose-driven spending, where everything from the products you buy to the credit cards and bank accounts you hold says something about your personal and financial preferences.

This puts more data in the hands of fintech startups, enabling them to leverage that data to provide more tailored solutions. It also calls for the need to market your financial services to a specific and narrowly defined market segment, positioning you as the market leader.

So what does that all lead up to? Financial institutions of the bygone era focused on capturing the broadest possible market to recoup massive fixed costs. The new generation of fintech startups, digital banks, and bank-fintech hybrids can create hyper-personalized and niche services that call out to specific customers. Let’s take a look at some examples:

Hyper-personalization and the evolution of fintech

Thanks to AI, it’s now possible to develop narrowly-defined solutions that serve highly specific individual needs.

Technology also enables the industry to reach out to traditionally underserved segments of the financial market, such as people with poor credit histories or seniors with piling healthcare costs. Let’s take a closer look at some ways fintech is developing highly tailored solutions to serve specific market segments:

Payment gateways

Payment gateways—platforms that enable merchants to accept payments online—are the lifeblood of ecommerce. They allow providers to charge for their products and services using various payment methods, from credit cards to online transfers to cryptocurrency payments.

By integrating different payment options into a unified user interface that buyers can easily access, payment gateways tap into the lucrative market that is ecommerce from various angles. They range from catch-all solutions like Stripe and Paypal to tailored payment gateways such as Braintree for startups and Square for brick-and-mortar businesses.

How does your mobile engagement score stack up?

Digital insurance providers

By offering aggressively cheaper rates than traditional insurance providers, fintech startups are disrupting the insurance industry with new solutions tailor-made for the digital age. InsurTech startups blend their unconventional business models with highly personalized marketing campaigns to reach specific market segments.

For example, Lemonade is a digital insurance company that takes a flat fee out of your premium and uses the rest to pay claims and donate to charity. It combines the prospect of cheap premiums and quick enrollment with a tangible social impact to create a unique fintech offering.

Investing and asset management

What if you could trade stocks without paying commissions to third parties?

Robinhood is a financial services company headquartered in Menlo Park that specializes in commission-free investment in stocks and cryptocurrency. Instead of charging commissions on each transaction, Robinhood makes money by selling investors’ trading data to high-frequency trade firms. While that may sound alarming to some, the shared data is not sensitive, and this is common practice among most investment firms and brokerage services.

Digital banking services

Imagine just how much banks could save if they didn’t have to invest in brick-and-mortar real estate and worked with half the staff—all without sacrificing the customer experience.

Jumpstarted by the pandemic, the digital banking industry has grown by leaps and bounds with a renewed focus on seamless automation and customer satisfaction. Digital banks such as Nu, Revolut, and N26 come with all the reliability and benefits of a physical bank. However, they can also offer reduced rates thanks to a marked reduction in infrastructural expenses.

Peer-to-peer funding

Instead of borrowing money from a traditional financial institution, peer-to-peer lending enables pre-approved borrowers and lenders to connect directly and exchange money via a secured platform.

Peer-to-peer funding is especially popular among startups at the investment readiness stage and small business owners, who can use the platforms to generate additional capital or maintain business cashflows through small loans. A few exciting operators in this space include Funding Circle and Kiva.

The rise of the social+ model in fintech

Social+ is a business model combining community with functionality to create a product that’s categorically social. Many companies use social media to promote their offerings, but social+ companies stand out because the product’s success is tied to the community built around it.

Social+ products enable consumers to engage with like-minded individuals in the context of the goal they’re trying to achieve, bootstrapping a loyal customer base that also serves as a network for further promoting your business.

However, a loyal customer base isn’t the social+ model’s only upside. Social+ products are a great resource for collecting data that enables you to understand your customers better. Learning more about your customers’ goals, aspirations, and pain points will help you further tweak and improve upon your existing product to better target specific user segments.

In fintech, social+ companies are creating a sense of belonging for investors and consumers and enabling them to share the ups and downs of their financial journey with an empathetic community. All the while, they’re also using this model to funnel their growth as financial data platforms.

Similar to Robinhood, Public.com is a commission-free stock brokerage platform and a great example of the rise of the social+ model in fintech. Public.com helps users make more informed decisions when engaging in stock trading while participating in a community that’s currently over two million strong.

Another excellent example of the social+ model in fintech is PayTM, India’s leading digital wallet and payment gateway app. PayTM recently partnered with Sendbird to build an in-app social experience to engage its users while they participate in financial transactions. Since its partnership with Sendbird, PayTM has sent more than 1 billion messages using Sendbird’s API.

Boost transactions with social interactions

PicPay uses Sendbird to embed a social engagement layer for users of its mobile payments app. PicPay found that the network effects from its social experience increased the number of transactions and average spending.

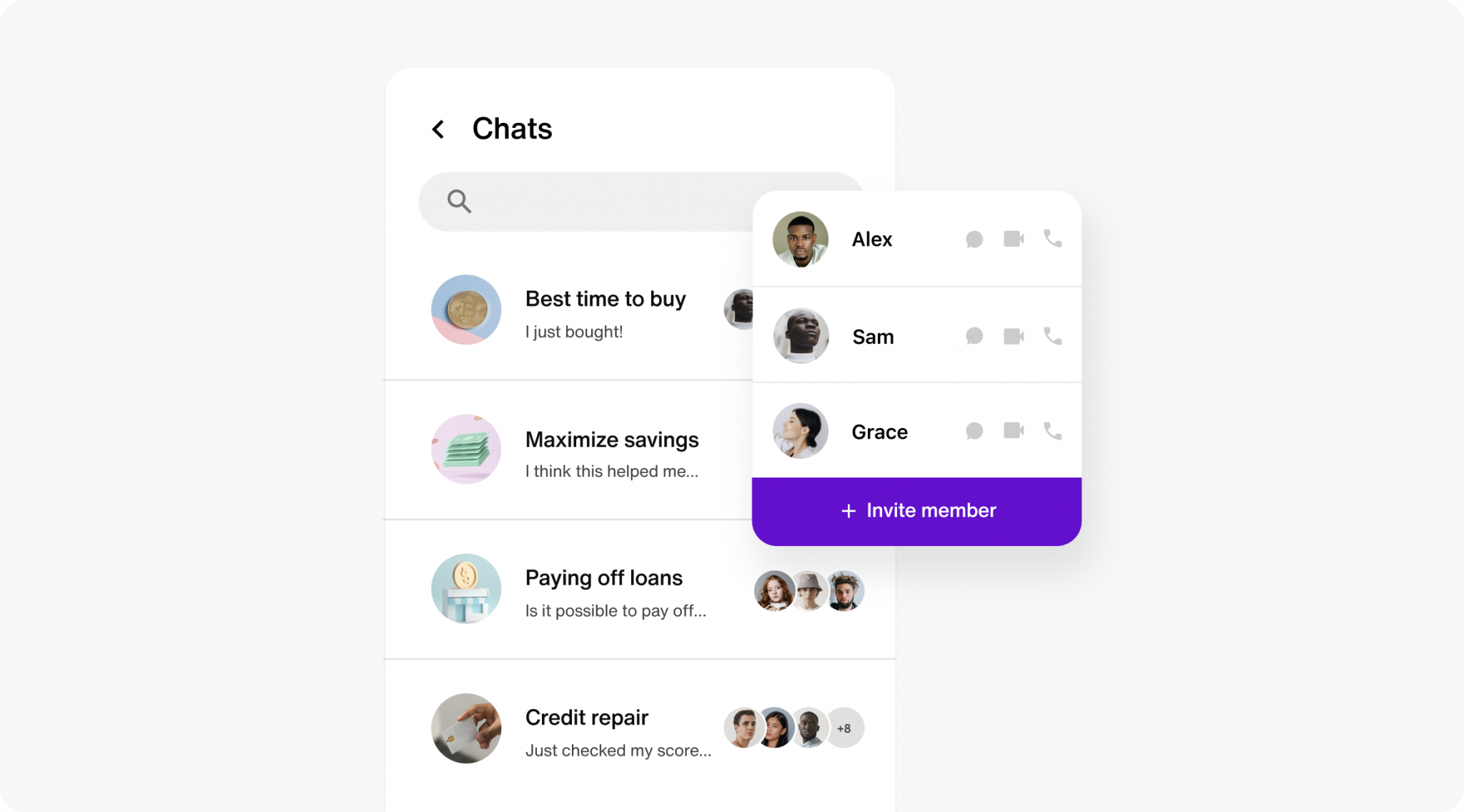

Personalize banking with in-app conversations

Building a social+ product from scratch isn’t easy. You’ll need a system that seamlessly integrates powerful social networking features with your product offering, which is very difficult to achieve in-house.

Sendbird is a social engagement platform that uses its proprietary API to deliver seamless social experiences within your mobile app. It saves you the trouble of building an entire social platform from scratch while also giving you the flexibility to create a social experience that suits your unique brand.

From Reddit to PayTM to Headspace, Sendbird’s easy-to-use Chat API and Chat SDKs have enabled app developers to integrate social networking features natively into their software. And in addition to in-app messaging experiences, Sendbird also specializes in voice and video calling features to empower your community further.